The IFRS Foundation began its work over 20 years ago developing voluntary international accounting standards through its International Accounting Standards Board (IASB). More than 140 jurisdictions around the world require that companies use the IFRS Accounting Standards in their financial reporting. The ISSB was created as a “sister board” to IASB and is responsible for developing and maintaining a “comprehensive global baseline of disclosure standards to facilitate consistent and comparable disclosures on risks and opportunities related to sustainability and climate”— namely, the IFRS Sustainability Disclosure Standards or what we will call here the ISSB Standards.2

The ISSB has four main objectives:

- to develop standards for a global baseline of sustainability disclosures;

- to meet the information needs of investors;

- to enable companies to provide comprehensive sustainability information to global capital markets; and

- to facilitate interoperability with disclosures that are jurisdiction-specific and/or aimed at broader stakeholder groups.

To help companies, the ISSB launched an online Knowledge Hub and a Sustainability Disclosure Taxonomy for digital tagging. Questions can be submit to the ISSB’s Transition Implementation Group (TIG).

- See this IFRS webpage for more details. Infographic adapted from the IFRS.

- MacCormac, Susan, Silva, Alfredo, and Onabanjo, Oluwabamise of Morrison Foerster LLP. (August 22, 2023). “Inside the IFRS S1 and IRFS S2 Sustainability Disclosure Standards.” Harvard Law School Forum on Corporate Governance.

Key Takeaways

There are several key concepts to understand before using the ISSB Standards, including how they compare with the Global Reporting Initiative (GRI) standards, the US Securities Exchange Commission (SEC) climate rule, and the European Union (EU)’s Corporate Sustainability Reporting Directive (CSRD).

How to use the standards

How does the ISSB define sustainability and materiality?

Using the IASB’s definition of material information, the ISSB Standards focus on financial materiality only:3

This Standard requires an entity to disclose information about all sustainability-related risks and opportunities that could reasonably be expected to affect the entity’s cash flows, its access to finance or cost of capital over the short, medium or long term… In the context of sustainability-related financial disclosures, information is material if omitting, misstating or obscuring that information could reasonably be expected to influence decisions that primary users of general-purpose financial reports make on the basis of those reports, which include financial statements and sustainability-related financial disclosures and which provide information about a specific reporting entity.

US companies may want to work closely with their legal and financial teams to understand how the ISSB’s definition of financial materiality may or may not differ from that of SEC rules. Such close collaboration may also be useful for those companies that may be subject to non-US jurisdictional reporting requirements that have or will adopt the ISSB Standards.

In addition to the ISSB’s definition of financial materiality, we suggest that companies may want to pay attention to its stipulation that for those disclosures involving a high level of judgment or uncertainty—including the identification of sustainability-related risks and opportunities and climate-related scenario analysis— a company use “reasonable and supportable information that is available to the entity at the reporting date without undue cost or effort.” The standards only allow omissions if laws or regulations to which a company is subject prohibit disclosing certain information or if information about an opportunity is commercially sensitive. A company needs to disclose if it is omitting information for these reasons and cannot use these exemptions to not disclose information about sustainability-related risks.

When do the ISSB Standards take effect? Can I still use the old TCFD recommendations and SASB standards?

The new standards—IFRS S1 and IFRS S2—are effective for annual reporting periods beginning on or after January 1, 2024. Reports covering 2023 data are the last to use the SASB industry standards and TCFD recommendations on their own.

- IFRS Foundation. (June 2023). IFRS S1 Disclosure Standard: General Requirements for Disclosure of Sustainability-related Financial Information. London, UK: pages 6 and 8.

Where should ISSB Standards disclosures be made?

The standards require that companies provide disclosures as part of their general-purpose financial reports. Companies are required to use consistent reporting boundaries, dates, data and assumptions to the extent possible between their sustainability-related financial disclosures and their related financial statements.

Companies are also asked to share what accounting sources of guidance they use in both (e.g., the IFRS® Accounting Standards or other applicable generally accepted accounting principles (GAAP) or practices).

Subject to any regulation or other requirements that apply, there are various possible locations in a company’s general-purpose financial reports in which to disclose information required by the ISSB Standards: management commentary, management’s discussion and analysis, operating or financial review, or in integrated reports, strategic reports, or similar financial reports. Information may also be included

by cross-reference to another report published by the company. Regardless of where the disclosures are shared, companies are asked to identify the financial statements to which their sustainability-related financial disclosures are related.

Finally, the ISSB notes that:

- Companies may disclose information in the same location as information disclosed to meet other requirements, such as information required by regulators.

- Sustainability-related financial disclosures should be clearly identifiable and not obscured by additional information.

- Companies should help users of its reporting understand the connections between their sustainability-related risks and opportunities and among the disclosures themselves.

What relief exists to help companies transition to the new disclosures?

To ease reporting burden, the ISSB has put in place temporary or permanent relief measures depending on a company’s circumstances. They include:

- Providing only climate-related disclosures the first year of use, though companies can provide disclosures for all their sustainability-related risks and opportunities.

- Omitting comparable information (i.e., prior year data) in its first year of using the standards, unless IFRS S1 or IFRS S2 state otherwise. If climate-only disclosures are shared the first year of use, then climate-only comparative information needs to be shared the second year of use.

- Providing qualitative rather than quantitative information about anticipated financial effects of a sustainability-related risk or opportunity if a company does not have the skills, capabilities or resources to provide quantitative information. The assumption is that those skills, capabilities and/or resources will be acquired over time to move towards quantitative information in future reporting.

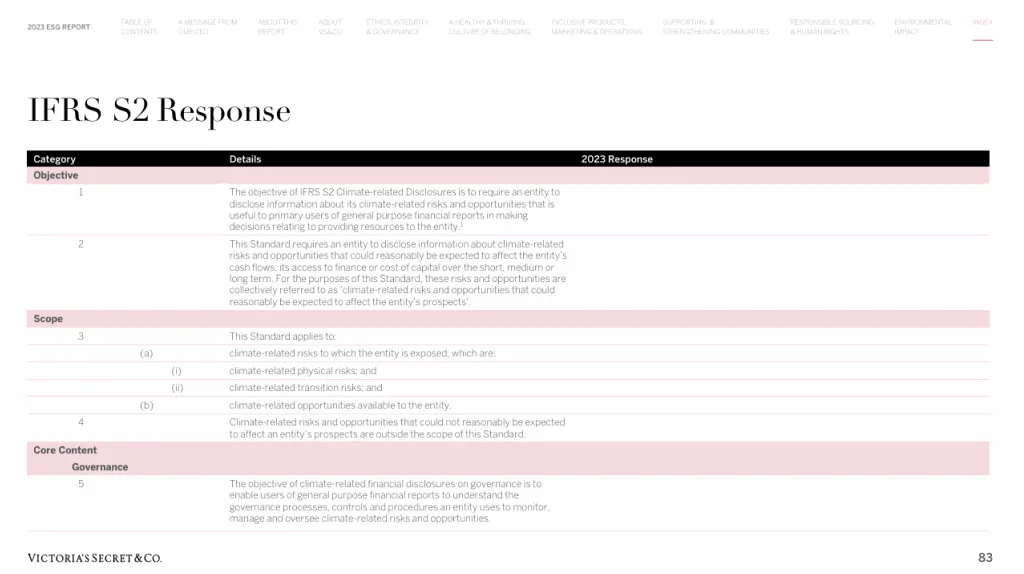

Victoria’s Secret & Co. is one of the only US companies to voluntarily move one year early from the TCFD recommendations to IFRS S2 in its 2023 ESG Report.

- Providing sustainability-related financial disclosures by half-year financial reporting instead of at the same time as annual financial statements, though still covering the same reporting period (e.g., prior fiscal year). This gives companies time to ensure third-party verification and assurance for key data.

- Continuing to use a non-Greenhouse Gas Protocol — A Corporate Accounting and Reporting Standard (GHG Protocol) measurement methodology the first year the standards are used. In addition, companies required by jurisdictional regulations to use an alternative GHG emissions measurement methodology are exempt from using the GHG Protocol.

- Not disclosing Scope 3 emissions the first year the standards are used. This includes relief from the requirements for companies that have asset management, commercial banking or insurance activities to provide additional information about financed emissions.

In what countries are the IFRS Sustainability Disclosure Standards becoming required?

As of June 2024, the International Organization of Securities Commissions (IOSCO) ⎯of which the SEC is a member alongside 129 other capital market authorities⎯had endorsed the ISSB Standards. In addition, more than 20 jurisdictions had announced publicly that they planning to incorporate or align their own standards with the ISSB Standards. According to the IFRS Foundation, these jurisdictions account for over 50% of global gross domestic product (GDP), more than 40% of global market capitalization, and more than 50% of global greenhouse gas emissions.4 Countries adopting or aligning with the ISSB Standards include Australia, Brazil, Canada, the European Union (as part of its Corporate Sustainability Reporting Directive (CSRD)’s European Sustainability Reporting Standards (ESRS)), Hong Kong, India, Japan, Malaysia, Mexico, New Zealand, Nigeria, Pakistan, the Philippines, Singapore, South Korea, Türkiye, and the United Kingdom (UK). Some jurisdictions are adding their own additional requirements on top of what the ISSB Standards require. The IFRS maintains a list of ongoing and completed jurisdictional consultations at the national or supra-national level on its website.

- IFRS Foundation. (May 28, 2024). Jurisdictions representing over half the global economy by GCP take steps towards ISSB Standards.

Canada and the IFRS Sustainability Disclosure Standards5

In March 2024, the Canadian Sustainability Standards Board (CSSB) released the first draft of its corporate sustainability reporting standards, which are adapted from the ISSB Standards. If approved, the standards will become part of the Canadian Sustainability Disclosure Standards (CSDS). The standards include CSDS 1 General Requirements for Disclosure of Sustainability-related Financial Information and CSDS 2 Climate-related Disclosures.

While the CSSB Standards largely align with IFRS S1 and IFRS S2, Canadian-specific modifications include:

- Extending the voluntary adoption date from January 1, 2024 to January 1, 2025.

- Extending the ability to use climate-only standards for two years instead of ISSB’s one year. For those companies that voluntarily adopt the CSSB standards on January 1, 2025, they will not be required to disclose information on all sustainability-related risks and opportunities until the reporting period beginning on or after January 1, 2027.

- Extending the requirement to disclose Scope 3 emissions for two years instead of ISSB’s one year. For those companies that voluntarily adopt the CSSB standards on January 1, 2025, they will not be required to disclose Scope 3 emissions until the reporting period beginning on or after January 1, 2027.

The Canadian Securities Administrators (CSA) have stated that they will be considering the public feedback received on the CSSB’s draft standards as they issue a proposal for a revised rule setting out climate-related disclosure requirements for Canadian companies. While any climate-related rule issued by the CSA will be required, the CSSB standards will remain voluntary.

- Marsh, Sarah, Morrison, Scott and Lawson, Jennifer. (March 14, 2024). “Canada’s Draft Sustainability Disclosure Standards.” PwC Canada.

Structure and details of the standards

What is the basic structure of the new standards?

The new IFRS S1 and IFRS S2 standards use the same overarching framework of the TCFD recommendations: namely, disclosures related to governance, strategy, risk management, and metrics and targets. IFRS S1 asks companies to disclose information under these four “buckets” for all financially material sustainability-related risks and opportunities, whereas IFRS S2 focuses on climate only.

Overview of IFRS S1 and IFRS S2 Requirements6

In addition to addressing general cross-industry requirements in IFRS S1 and IFRS S2, companies need to address industry-based requirements. The ISSB requires that companies review applicable SASB Standards to help them identify risks, opportunities, metrics, targets and disclosure requirements not outlined in

IFRS S1 and IFRS S2. In addition, companies are encouraged to look at applicable regulations; the water and biodiversity-related disclosure guidance from the former Climate Disclosure Standards Board (CDSB); any recent pronouncements from investor-focused standard-setters; and sustainability-related risks and opportunities identified by companies that operate in the same industries or geographic regions. Finally, companies are encouraged to look to the GRI Standards and the European Sustainability Reporting Standards (ESRS) for possible applicable disclosure requirements.

- Infographic adapted from Deloitte. (June 30, 2023). “Global ESG Disclosure Standards Converge: ISSB Finalizes IFRS S1 and IFRS S2.” #DeloitteESGNow, Volume 30, Issue 11.

Role of SASB Standards in IFRS S1 and IFRS S27

What are the requirements of IFRS S1 General Requirements for Disclosure of Sustainability-related Financial Information?

IFRS S1 requires a company to disclose complete, neutral and accurate (in IFRS’s words “fair”) information representative of all its financially material sustainability-related risks and opportunities across its entire value chain. The required disclosures are grouped into the “buckets” of governance, strategy, risk management, and metrics and targets.

When a company uses the same risk management process to identify, assess, prioritize and/or monitor different sustainability-related risks and opportunities, it can integrate its disclosures for all its financially materially topics rather than providing separate disclosures for each sustainability-related risk and opportunity.

Two final requirements under IFRS S1 merit attention. IFRS S1 requires information about current and anticipated financial effects of sustainability-related risks and opportunities. In addition, it requires an “explicit and unreserved statement of compliance” along with the disclosures. Companies can only claim compliance if they meet all requirements of the standard.

What are the requirements of IFRS S2 General Requirements for Disclosure of Climate-related Financial Information?

IFRS S2 follows closely the former TCFD recommendations. Companies are asked to share details on their governance, strategy, risk management, and metrics and targets related to their climate risks and opportunities.

Companies are also asked to review industry-specific climate guidance to help identify climate-related risks, opportunities, metrics, targets, and other disclosures. Companies are still required to conduct climate-related scenario analyses to identify and prioritize their short, medium and long-term risks and opportunities. Where companies have similar information for IFRS S2 as they would for IFRS S1, they can integrate those disclosures for IFRS S2 into IFRS S1.

The IFRS Foundation has released more detailed information comparing IFRS S2 with the TCFD recommendations.

- Infographic adapted from IFRS Foundation. “SASB: Your pathway to ISSB.”

Comparisons with other sustainability reporting regulations or voluntary standards

While the ISSB Standards were developed to align or be interoperable with several other sustainability reporting regulations and voluntary standards, there are key differences.

| IFRS (ISSB Standards) | SEC ESG-Related Rules | GRI | CSRD’s ESRS | |

|---|---|---|---|---|

| Audiences | Investors and readers of financial reports | Investors and readers of financial reports | Broad range of stakeholders | Broad range of stakeholders |

| Materiality | Financial | Financial (non-ESG) | Impact | Double; uses same or similar financial definition as IFRS and impact materiality definition as GRI |

| Topics in scope | E, S and G topics Climate for all |

Human Capital Management Cybersecurity Climate |

E, S and G topics | E, S and G topics Climate for all |

| Industry standards | SASB standards, which will be revised over time | None | Sector-specific standards released and in development | Sector-specific standards in development |

| Location of disclosures | Included as part of general purpose financial reporting, such as in management commentary, but flexible on location. No financial statement footnote required |

Climate rule (stayed): included in separate section of annual report or registration statement Climate rule (stayed): financial statement footnote to include disclosure of impact of severe weather and transition-related activities |

ESG or Sustainability report GRI content index |

Included within dedicated section of management report No financial statement footnote required |

| Emissions and Assurance | Scopes 1, 2 and 3 Defers to jurisdictional requirements |

Scopes 1 and 2 (if material) Limited to Reasonable assurance over time |

Scopes 1, 2 and 3 Recommends assurance |

Scopes 1, 2 and 3 Limited to Reasonable assurance over time |

| Timing | 2025 covering 2024 data though can use now | HCM and cybersecurity in use now Climate on hold but could be phased in starting in Fiscal Year 2025 |

In use now with updated energy and climate topic standards coming 2025 | Depends on location and size Non-EU headquartered companies and certain industries in 2026 |

How does IFRS S2 compare to the former TCFD recommendations?

IFRS S2 is very similar to the former TCFD recommendations. However, IFRS S2 requires climate-related information be included in annual financial statements, whereas companies tended to include disclosures that followed the TCFD recommendations in their annual sustainability or environmental, social and governance (ESG) reports and/or in separate TCFD-focused reports. In addition, IFRS S2 asks for more information than the former TCFD recommendations in some key areas:

| New or Additional Requirements in IFRS S2 Compared to TCFD Recommendations | |

|---|---|

| Governance |

|

| Strategy |

|

| Risk Management |

|

| Metrics and Targets |

|

How does IFRS S2 compare to the proposed SEC climate rules?

While the SEC climate rule is currently being held pending court review, it may still be worth noting the similarities and differences between the rule and IFRS S2.

The main differences include:

| SEC Climate Rule | IFRS S2 | |

|---|---|---|

| Governance |

|

|

| Strategy |

|

|

| Risk Management |

|

|

| Metrics and Targets |

|

|

|

|

|

|

|

|

|

|

|

|

|

How does IFRS S2 and the full ISSB Standards compare to the CDP annual questionnaire?

In June 2024, CDP launched a new, streamlined online reporting platform that combines its formerly separate climate, forests, water, biodiversity and plastics environmental questionnaires into one questionnaire and dataset. As part of this streamlining, CDP purposely aligned its questionnaire with other international frameworks and standards:

- CDP’s foundational climate questions now align with IFRS S2.

- CDP’s biodiversity questions now align with the recommendations of the Taskforce on Nature-related Financial Disclosures (TNFD).

- CDP has aligned many of its questions with the CSRD’s European Union standards (ESRS).

A record 75,000 companies were asked to disclose environmental information to CDP when the new platform was launched. CDP also released a questionnaire for small and medium-sized enterprises (SMEs) tailored to their needs and resources.⁸

How do the ISSB Standards compare to the EU’s European Sustainability Reporting Standards (ESRS) under its Corporate Sustainability Reporting Directive (CSRD)?

The ISSB, the European Commission services, and the European Financial Reporting Advisory Group (EFRAG) released ESRS-ISSB Standards Interoperability Guidance in 2024. At a high level:

- Along with sharing other commonly defined terms, the ESRS use the same definition of financial materiality as that in IFRS S1.

- Nearly all the climate-related disclosures in the ISSB Standards are included in the ESRS.

- Finally, the ESRS are listed as part of the ISSB Standards’ general requirements appendix as a source of guidance companies may consider, in the absence of a specific ISSB standard, to identify metrics and disclosures if they meet the information needs of investors.

Some key differences include:

- ESRS E1 does not (yet) require disclosure of financed emissions, but future ESRS sector-specific standards could. ESRS E1 does include a requirement to follow ISSB provisions if a company concludes these are material.

- ESRS E1 requires only gross emission reduction targets and does not allow inclusion of GHG removals, carbon credits or avoided emissions as a means of achieving targets. Companies are required to share carbon credit details only if they are being used as part of already existing carbon neutrality (net target) public claims.

- ESRS E1 requires that companies clearly identify additional disclosures (e.g., those meeting ISSB or GRI requirements) with reference to the non-ESRS legislation, standard or framework being referenced and still follow ESRS requirements for qualitative characteristics of information.

How do the ISSB Standards compare to the Global Reporting Initiative (GRI) standards?

The main difference between the standards is the type of materiality lens used: the ISSB Standards focus on financial materiality only, while the GRI Standards focus on impact materiality only—namely, a company’s most significant impacts on the economy, environment, and people (incorporating human rights), including how an organization manages these impacts, regardless of financial implications.

GRI and the ISSB have been working closely together since 2022 to advance the complementarity and interoperability of their respective standards. For example:

- In January 2024, the IFRS Foundation and GRI published “Interoperability considerations for GHG emissions when applying GRI Standards and ISSB Standards.” The guidance discusses areas of interoperability between GRI 305: Emissions and IFRS S2. As the GRI energy and climate topic standards are being revised, updated guidance is anticipated in 2025.

- In 2023, GRI and the IFRS Foundation launched the Sustainability Innovation Lab (SIL) to bring together global and local partners to advance capabilities for reporters using both the GRI Standards and the ISSB Standards.

GRI and the ISSB anticipate releasing more guidance on how to use both sets of standards over time.

Citations

Bichet, Emma, Mencher, Michal, and Sasfai, Beth, Cooley LLP. (April 15, 2024). “Comparing the SEC Climate Rules to California, EU and ISSB Disclosure Frameworks.” Harvard Law School Forum on Corporate Governance.

CDP. (June 5, 20240.) Financial institutions with a record $142 trillion in assets demand climate and nature data, as CDP unveils new disclosure platform.

Deloitte. (June 30, 2023). “Global ESG Disclosure Standards Converge: ISSB Finalizes IFRS S1 and IFRS S2.”

#DeloitteESGNow, Volume 30, Issue 11.

EFRAG Secretariat. (August 23, 2023). “Paper 04-02: Interoperability between ESRS and ISSB standards: EFRAG assessment at this stage and mapping table.” EFRAG SRB Meeting.

Financial Reporting & Assurance Standards Canada. (March 13, 2024). Canadian Sustainability Standards board Announces First Canadian Sustainability Disclosure Standards for Public Consultation.

Global Reporting Initiative. (June 26, 2023). “Progress towards a strengthened sustainability reporting system.”

IFRS Foundation. (July 2023). “Comparison IFRS® S2 Climate-related Disclosures with the TCFD Recommendations.”

IFRS Foundation. (June 2023). IFRS S1 Disclosure Standard: General Requirements for Disclosure of Sustainability-related Financial Information.

IFRS Foundation. (June 2023). IFRS S2 Climate-related Disclosures.

IFRS Foundation. (June 2023). “Project Summary: IFRS® Sustainability Disclosure Standards.”

IFRS Foundation. (May 28, 2024). Jurisdictions representing over half the global economy by GCP take steps towards ISSB Standards.

IFRS Foundation and Global Reporting Initiative (GRI). (January 2024). “Interoperability considerations for GHG emissions when applying GRI Standards and ISSB Standards.”

MacCormac, Susan, Silva, Alfredo, and Onabanjo, Oluwabamise of Morrison Foerster LLP. (August 22, 2023). “Inside the IFRS S1 and IRFS S2 Sustainability Disclosure Standards.” Harvard Law School Forum on Corporate Governance.

Steward, Dr. Mary; Kember, Olivia; Evans, John; Catchpole, Stephen; and Wood, Dr. Nick. (September 18, 2023). “IFRS S2 requirements relative to TCFD recommendations. How will climate disclosures change?” Published by Energetics on LinkedIn.

Stewart, Neil. (January 19, 2023). “Future of the SASB Standards: What you need to know for 2023 disclosure.”

US Securities Exchange Commission. (March 6, 2024). “SEC Adopts Rules to Enhance and Standardize Climate-Related Disclosures for Investors.”